Richard Hillson

Richard Hillson

The Alternative Source: SEI Welcomes the SEI Altigo® Platform

We kicked off our new video series, The Alternative Source, with Kevin Crowe, Senior Vice President, and Mat Dellorso, Managing Director, as they...

The following is a guest post by Richard Hillson of Hillson Consulting:

Venture debt is a term that you may not have heard, but it is certainly one you will hear more of in the near future. The little brother of traditional equity, venture capital is eating into the market share and the numbers show considerable growth.

Venture debt consists of secured floating-rate loans, typically with a three-to-four-year maturity, used as growth capital by companies who have already received institutional equity funding. In addition to interest (coupon) payments, the return will typically include equity participation through warrants. This allows the lender or investor in the fund to potentially benefit from equity upside in a debt transaction.

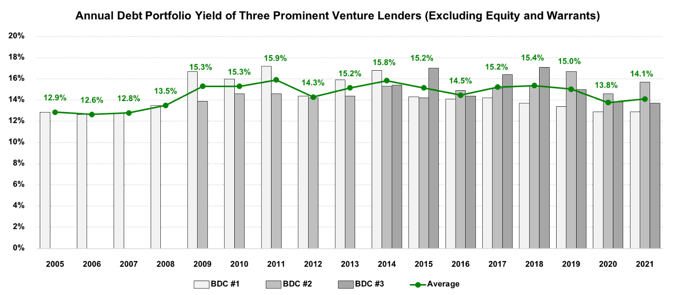

Venture debt lenders have consistently produced a 15-20% return over the past 20 years. The debt yield has been approximately 15% annually (in a low interest rate environment) with equity returns equal to another 3% to 5% on average each year. The default rate in the industry is surprisingly low and recovery rates are typically above 80% on defaulted loans. Thus, annual average losses are less than 0.50% based on public SEC filings and industry analysis performed by Applied Real Intelligence (A.R.I.), a Los Angeles-based venture lender.

*Source: A.R.I. analysis of SEC filings of publicly traded Business Development Companies (BDCs)

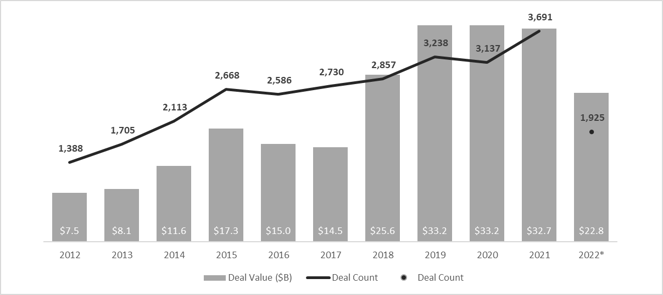

Investment in innovation has been growing exponentially. In 2021, venture capital (“VC”) deal activity in the U.S. reached a record $344 billion, more than two times the previous record of $169 billion set in 2020*.

The size of the venture debt market is more than $30 billion annually in the U.S., having grown more than 4x growth in the past decade. Venture debt financing has accounted for approximately 10% of the total venture funding in the U.S. over the last several years. We have seen some high-profile transactions in venture debt, involving household names like AirBnB, Draft Kings, Impossible Foods, Evernote, and DoorDash.

*Source: PitchBook-NVCA Venture Monitor, Q3 2022”. Pitchbook and National Venture Capital Association (NVCA), October 2022

There are various risks to consider in relation to venture debt. A few of the most commonly asked questions that should be explored during due diligence include:

As soon as a client hears “venture”, the assumption is immediately that of higher risk and more volatile exposure. I spoke with Zack Ellison, CFA, CAIA, the Managing General Partner and CIO of A.R.I.’s Venture Debt Opportunities Fund, to gain deeper insights into venture debt’s risk profile.

Typically, lenders in the venture debt space will mitigate their risk in a number of ways:

Venture debt should be considered more like private credit rather than venture equity in terms of its risk profile. Venture debt provides equity-like returns with the risk of senior secured debt.

Venture debt has fared consistently well through market cycles including the Global Financial Crisis of 2008 – 2010 and seven market corrections (defined technically as a major index falling by more than 10% from its recent high) from 2010 through 2021. Given its focus on funding tech and tech-enabled companies, venture debt performed very well in 2020 and 2021 despite the impact of the global COVID-19 pandemic.

“Over the past two decades, venture debt has consistently produced annual returns in the 20 percent vicinity with minimal losses, very low volatility of returns, and limited correlation to other assets. The current opportunity is the best we have ever witnessed given significant demand for capital and limited supply as VCs and banks scale back,” said Ellison.

Venture debt is complementary to venture equity and is not a substitute. The largest part of a venture lender’s deal flow comes directly from VCs who oftentimes directly connect lenders with their portfolio companies that are the best candidates for venture debt.

When analyzing why a founder would choose debt financing over equity in the venture world there are a few key advantages:

“Ultimately, we find that 100% of founders will utilize debt in conjunction with equity when given the opportunity. Venture debt accelerates growth and extends runway while also helping founders maintain greater ownership in the companies they have built,” said Ellison.

Devastating losses in the bond market in 2022 have left investors looking for solutions. Corporate bonds that are fixed rate have both credit risk and interest rate risk. Rising interest rates have led to declining bonds values. If the economy worsens, credit spreads will also start to widen. In an attempt to counteract these risks, investors are moving to floating-rate securities that are more senior in the capital structure and hence lower risk. Private credit, including senior secured loans with floating interest rates that offer double digit returns, has been a popular alternative of late.

“Absolutely—with the struggles of the 60/40 portfolio, most mainstream investors were down 20% to 25% in 2022. We’re seeing the most demand from RIAs, wealth advisors, and their clients who are seeking higher returns, greater safety, and low correlation to stocks, bonds, and other assets in their portfolios. For sophisticated investors and their advisors, venture debt should absolutely be considered as a better alternative to corporate bonds and other fixed-rate securities,” said Ellison.

It has long been the case that clients and advisors allocating to alternatives would take their alts slice from their equity portion of the portfolio, deeming it risk capital. I have long argued that alts should be segregated in a number of ways, including whether they are targeting equity returns or yield. Yield-focused alts should absolutely be considered as a replacement for underperforming fixed income and come from the “40” allocation, not the “60” allocation.

Private credit is an asset class which has certainly become more mainstream, and I will certainly be paying more attention to venture debt as a rapidly growing asset class that provides attractive risk-adjusted returns and significant diversification benefits.

Richard Hillson

Hillson Consulting is a boutique investment consultancy founded by financial services entrepreneur Richard Hillson. The company helps independent advisors enhance and improve their offerings and drive revenue through alternative investments. HC also works with product sponsors to help them with education and access within the independent RIA channel.

Zack Ellison

Applied Real Intelligence (A.R.I.) is a Los Angeles-based venture debt investment manager focused on providing financing solutions to innovative, high-growth, venture-backed companies in recession-resistant sectors and underserved regions in North America. As Managing General Partner of A.R.I. and CIO of A.R.I.’s Venture Debt Opportunities Fund, Zack Ellison, CFA, CAIA, is responsible for leading the firm’s management and investment activities.

We kicked off our new video series, The Alternative Source, with Kevin Crowe, Senior Vice President, and Mat Dellorso, Managing Director, as they...

SEI to Leverage Unique Industry Position to Meet Market Demand and Streamline Investment Process for Alternatives

Mike Consol, Editor at Real Assets Adviser, asked Bill Robbins, CEO at Altigo and WealthForge, to address the capabilities of straight-through...